HOME PRICE GROWTH AND CAN IT CONTINUE?

HOME PRICE GROWTH AND CAN IT CONTINUE?

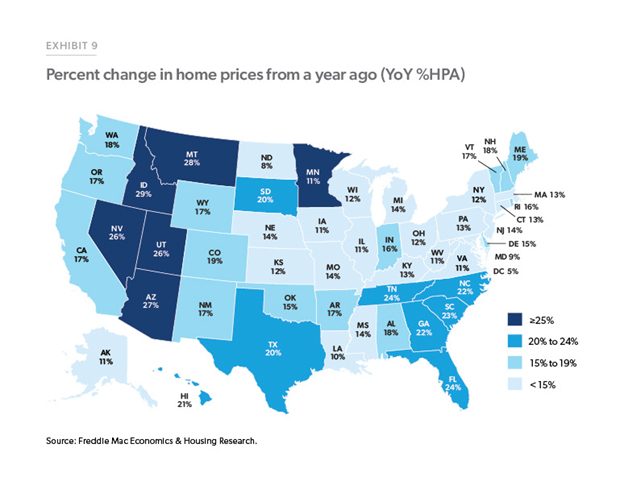

Home prices, the best single indicator of whether market conditions favor buyers or sellers, jumped 33% nationally over the past two years. What is behind the strength of the housing market, and can it continue?

FREDDIE MAC Sees it this way:

- record low mortgage rates in 2020 and 2021, and the race to beat future rate increases;

- limited supply from underbuilding and below average distressed sales;

- an increase in first-time homebuyers due to favorable age demographics; and

- increased migration from high-cost cities to areas that already had a housing shortage.

Record low mortgage rates

The pandemic resulted in the 30-year fixed-rate mortgage dropping from 4.6% at the end of 2018 to a record low of 2.7% at the end of 2020. Comparable declines relative to average rates from the prior three years are rare. That large of a drop in rates has only happened twice before in the past 20 years: in 2003 and after the housing bust in 2009. All three occurrences resulted in noticeably higher home price growth.

The supply of homes for sale was already at record lows before the pandemic

A housing shortage already existed pre-pandemic.1 The shortage was evident in both a record-low number of homes for sale and low vacancy rates. There is a strong correlation between “Months’ Supply” and home price growth.

When Months’ Supply fell below three months in 2020, it led to a surge in home prices. This led us to a reacceleration of home prices this spring.

At the same time that sales were increasing due to higher demand, the tight supply got even tighter as builders were slowed down by pandemic related issues and there were fewer distressed sales (both foreclosures and short sales).

Thanks to pandemic-related forbearance and foreclosure moratoriums, far fewer distressed sales came to market than would have otherwise. These programs provided time for home equity to accumulate due to rising home prices and for employment conditions to improve, suggesting that a significant number of foreclosures were permanently avoided.

Demand rose due to a record surge in first-time homebuyer purchases

Just as important as the limited new supply is the extraordinary demand from first-time homebuyers. Highly favorable age demographic trends may be the key to today’s housing market.

This demographic increase in potential homeowners was not met with enough new construction. Thus, vacancy rates dropped, pushing up rents and making renting less attractive.

There are now 18% more people between the ages of 25 and 34 than in 2006. The number of high-income renters who can afford to buy, and are of prime first-time homebuyer age, has also been growing.

Freddie Mac financed 554,000 first-time homebuyers in 2021, up 22% from 2020 and the highest level since tracking began in 1994. Despite higher home prices and record low supply, first-time buyers have added significantly to demand.

Migration South and West is redistributing home price growth to interior markets

The pandemic accelerated the pace of the migration out of large cities that has been occurring over the last two decades

Expanding work-from-home options accelerated a long-standing migration towards more affordable locations, many with attractive weather or natural amenities. We believe this trend will continue.

Remote workers and retirees moving to more affordable areas (relative to where they are coming from) should keep home price growth in these areas stable, since many of the new arrivals have the means to afford the now higher home prices in the areas to which they are moving.

What happens next?

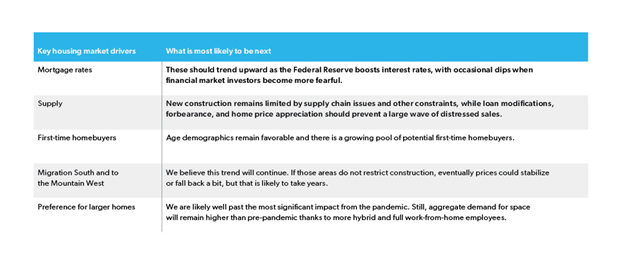

Here are some key housing market drivers:

The effect of increasing mortgage rates

According to Freddie Mac, the critical question of estimating the impact of rising rates on home prices suggests that a 1% increase in mortgage rates results in a little over four percentage points lower home price growth (for example, moving from 11% home price growth a year to 7%). In comparison, J.P. Morgan analysts estimate a more significant impact of roughly six percentage points lower home price growth. The housing market may be more sensitive now to higher rates than in the past since home prices have gotten so high.

While it is intuitive that higher rates cool demand by worsening affordability, the actual history is a far more nebulous guide to what will happen because there’s also a large offsetting effect—interest rates typically increase when the economy is strengthening.

Final Thoughts

As many aspects of the economy were still reeling from the worst health and economic crisis in a generation, the housing market demonstrated unprecedented strength and resilience. In addition to the dynamics of the pandemic itself, this strength was driven by increased demand precipitated by record low mortgage rates, a growing number of first-time homebuyers, and increased domestic migration.

If mortgage rates stabilize near today’s rates, all else equal, this estimate suggests far slower, yet positive home price growth with a wide geographic range based on migration patterns.

While higher rates are concerning, other key drivers are likely to remain benign. The housing market remains underbuilt and increased migration to lower-cost areas—often with warm climates or natural amenities—is expected to continue as work-from-home gets more entrenched. This matters since most booming areas already have a severe housing shortage due to a prior influx of new residents.

Finally, favorable demographics suggest that strong first-time homebuyer demand can continue. That is because there is still a significant number of younger renters who have enough income to support homeownership and they should remain a potent force for the foreseeable future.

Prepared by the Economic & Housing Research group

Sam Khater, Chief Economist

Ralph DeFranco, Macro Housing Economics Senior Director

Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.